In order to achieve any growth for your business nowadays, social media has got to be one of the most important factors in your marketing strategy. However, despite how helpful social media can be, it can still be quite a dangerous tool if not used carefully and effectively. Check out this piece I wrote on TechAndScience.com: http://techandscience.com/techblog/ShowArticle.aspx?ID=5323

Since the establishment of credit cards and easy payment on credit for normal, everyday transactions, many people have found that, while they may be convenient, credit cards can be a tremendous burden when misused. Those who are unfamiliar with the workings of credit cards can easily accrue hundreds and thousands of dollars of debt as interest accumulates on a purchase. While these people may most be in need of debt relief, unpaid credit card debt will continue to balloon, making repayment progressively more difficult.

In order to take control of the situation and begin paying off this debt, consider the following five tips for reducing and paying off credit card debt.

As such, the first step in reducing your credit card debt is to understand how you accrued this debt in the first place. To do so, track your spending for several weeks to determine and cut down on inappropriate uses of the card.

While budgeting does not mean that you must give up all unnecessary expenses, sacrifices must certainly be made in the interest of good financial health. Try to reduce your spending overall without making radical lifestyle changes unless necessary. Remember, a good budget is not just one that limits spending but also one to which you can adhere.

Generally, there are two methods for paying off credit card debt: paying off the highest interest card first or paying off the credit card with the lowest balance first. In either case, the most recommended strategy is to focus on paying off a single credit card, while paying the minimums on the other cards. Of these two methods, the first method tends to be the fastest and most cost-effective, since high-interest credit cards will be the most troublesome culprits in causing and prolonging this debt.

This strategy is only recommended to those who are confident that they will be able to repay the balance on time; those who cannot pay off the transferred balance by the end of the billing cycle may end up with even higher interest rates than had they on their old card. Since credit card debt typically stems from bad financial habits, it is recommended that those already in credit card debt avoid such a risky solution; however, for those who can repay the balance, this method can be incredibly beneficial.

Once you have seen some results from your repayment strategy and you have successfully reduced your unnecessary spending, it may be time to treat yourself. As previously mentioned, a budget does nothing unless you can be motivated to stick with it, so do not be afraid to splurge once in awhile, within reason. Seeking the help of a professional debt relief service such as National Debt Relief can also be a way to turn to proactively battle debt entanglements. In conclusion, credit card debt can be a hefty burden to carry, but there are ways to counteract this debt. Ultimately, the best way to lower your credit debt is to practice better spending habits and to be aware of your credit balance at all times. Remember, at the end of the day, reducing your credit card debt will not be a simple, one-time fix but will require an adjustment of financial habits over a long-term, but by learning and practicing these habits, you can defeat your debt once and for all.  Long before the internet revolution, computer manufacturers and teachers alike angled for ways to take advantage of computers in the classroom. Beginning in the early 1980’s—the dawn of affordable consumer-end personal computers—software designers sought to harness digital technology to present students with a stimulating, interactive approach to learning.

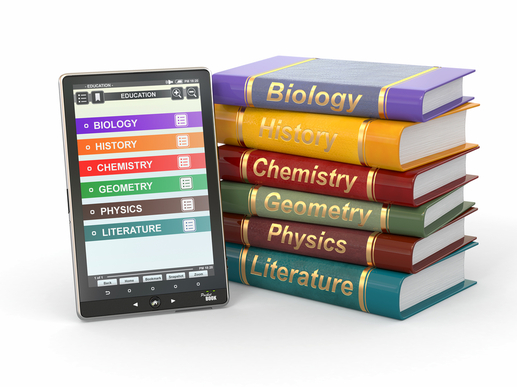

Now, however, high-speed, highly portable electronic devices present far more radical promise than a few hours of Oregon Trail in the computer lab. It’s now possible for handheld tablets to supplant traditional paper materials both in the classroom and at home, but is such a massive transition a good idea? Here are the major talking points in the tablet vs. textbook conversation: Material realities Not surprisingly, the same issues that have set the publishing world on its head are at stake in the domain of print vs. digital: the physicality of books has huge ramifications. At the front and center of the debate are environmental issues, of course, but the nature of traditional classroom education makes this an even more runaway problem. Why? First of all, educational materials, by definition, have a built-in expiration date. Even among relatively static subjects—algebra, let’s say—textbooks tend to be revised annually, making older editions obsolete. Unlike a used novel, a textbook is not likely to have a second life for this very reason. Handouts and other generated supplements only make matters worse. On the other hand, there are less obvious environmental drawbacks to using tablets. While they may eschew demands to our world’s forests, according to The New York Times, a tablet or other e-reader may be guilty of being 70-times as deleterious to the planet as a single textbook, due to both the extraction of minerals and energy expended in production. The tangible quality of textbooks brings up more concerns than just the environment, however. Every textbook tends to be a bulky, unwieldy tome, and a busy student’s schedule usually requires that he or she carry more than one at a time. The burden is more than just annoying; it’s actually a health hazard. Especially in younger people whose bones have yet to mature, carrying from 10 to 30% of one’s body weight, as is common among students, can lead to scoliosis and chronic lower back pain. Tablets, on the other hand, can pack in more material than students are likely to read in their lifetimes. Fiscal factors There’s no contest in the debate over the space-conserving potential of using tablets in lieu of print materials, but the controversy over whether they will save money is just getting started. On the one hand, a study by the FCC suggests that once the average price of tablets drops to $150, we’ll save over $3 billion per year. However, that’s only budgeting for the raw materials alone; such a projection does not account for the administrative retrofitting, training, and infrastructural updates that will enter the picture. Even if down the road the collective tablet-based educational budget should shrink below the current paper-based one, we should still expect an initially egregious start-up investment, such critics are saying. Furthermore, there are regional and class considerations. It may take time for already-strapped school districts to afford the initial bid, while low-income students may not have the internet capabilities at home for tablet-based homework. Effectiveness Above all of these questions, the bottom line should be whether or not our children will actually learn through tablets. Current studies give a fairly clear answer of yes and no. On the one hand, students prepped with tablets are able to outperform on standardized tests. Perhaps, because of today’s Information Age children develop alongside computers already, they also absorb more information more quickly. The downside is that tablet-based students are more likely not to retain that information for long. This may be because school districts already using tablets may endorse the kind of quantitatively-driven policies that result in “cram-and-forget,” test-centric studying. People who use print text, on the other hand, understand more and retain knowledge more permanently. As one may surmise, some of the statistics above may result not from any intrinsic qualities of the two competing media, but from cultural norms that have formed around them. Students may equate computers with endless leap-frogging of hyperlinks, for example, creating a built-in attention deficit in the learning process. Additionally, there are practical concerns for which tablets still have no answer: delicate, glitch-prone technology can’t compete with the ruggedly low-tech hard copy, and teachers can surely expect to hear choruses of “the dog ate my charger.” Nevertheless, even if the final result is a complementary relationship between the two, it’s unlikely that tablets will disappear from our schools. | ArchivesCategories |

RSS Feed

RSS Feed